Crown Holdings Declares $0.35 Dividend, 35% Increase

Crown Holdings announced that its Board of Directors declared a cash dividend of 35c per share, payable March 31, 2026, to shareholders of record as of March 17, 2026. This quarterly dividend represents an increase of 35% over the previous dividend of 26c per share. Timothy J. Donahue, Chairman, President and Chief Executive Officer, stated, "Our 35% dividend increase underscores the strength of our earnings and free cash flow generation, the resilience of our end markets, and our confidence in our operations. Supported by our solid balance sheet, we are well-positioned to consistently return capital to shareholders. We remain committed to our balanced capital allocation framework - maintaining our net leverage ratio at approximately 2.5x, investing prudently to support long-term growth, paying a sustainable and growing dividend, and returning capital through disciplined share repurchases."

Trade with 70% Backtested Accuracy

Analyst Views on CCK

About CCK

About the author

Crown Holdings Announces 34.6% Increase in Quarterly Dividend

- Dividend Increase: Crown Holdings has declared a quarterly dividend increase from $0.26 to $0.35 per share, representing a 34.6% rise, which reflects the company's robust cash flow and profitability, thereby boosting investor confidence.

- Yield Metrics: Following this adjustment, the forward yield stands at 1.22%, which not only attracts income-seeking investors but also supports the company's performance in the capital markets.

- Shareholder Benefits: The dividend will be payable on March 31, with a record date of March 17 and an ex-dividend date also set for March 17, ensuring shareholders receive timely returns and reinforcing the relationship between the company and its investors.

- Future Projections: Crown Holdings projects earnings per share of $7.90 to $8.30 for 2026 while targeting $900 million in free cash flow through capacity expansions, demonstrating the company's confidence in future growth and strategic positioning.

CROWN HOLDINGS INC ANNOUNCES $0.35 PER SHARE CASH DIVIDEND PAYABLE ON MARCH 31, 2026

- Dividend Announcement: Crown Holdings Inc. has declared a cash dividend of $0.35 per share.

- Payment Date: The dividend is scheduled to be payable on March 31, 2026.

Amcor's Strategic Outlook Post-Berry Global Merger

- Merger Impact: Amcor's all-stock merger with Berry Global, completed last April, is projected to generate approximately $23 billion in revenue over the next twelve months, and if profit margins return to levels seen three years ago, net income could exceed $1.85 billion, highlighting the scale benefits and market potential of the merger.

- Earnings Guidance: Management has guided for adjusted earnings per share of $4.00 to $4.15 for FY2026, with free cash flow expected to be between $1.8 billion and $1.9 billion, indicating a strong financial outlook post-merger that could enhance investor confidence.

- Debt Management Risks: While the company aims to reduce its debt levels of approximately $15 billion, the current debt-to-EBITDA ratio stands at 4x, indicating potential operational leverage risks when paying down debt, especially as packaging demand may soften.

- Dividend Appeal: With a dividend yield of 5.24%, Amcor offers relative attractiveness in the current market, and while dividend payments may impact option pricing, the stable cash flow and dividend policy still provide value support for investors.

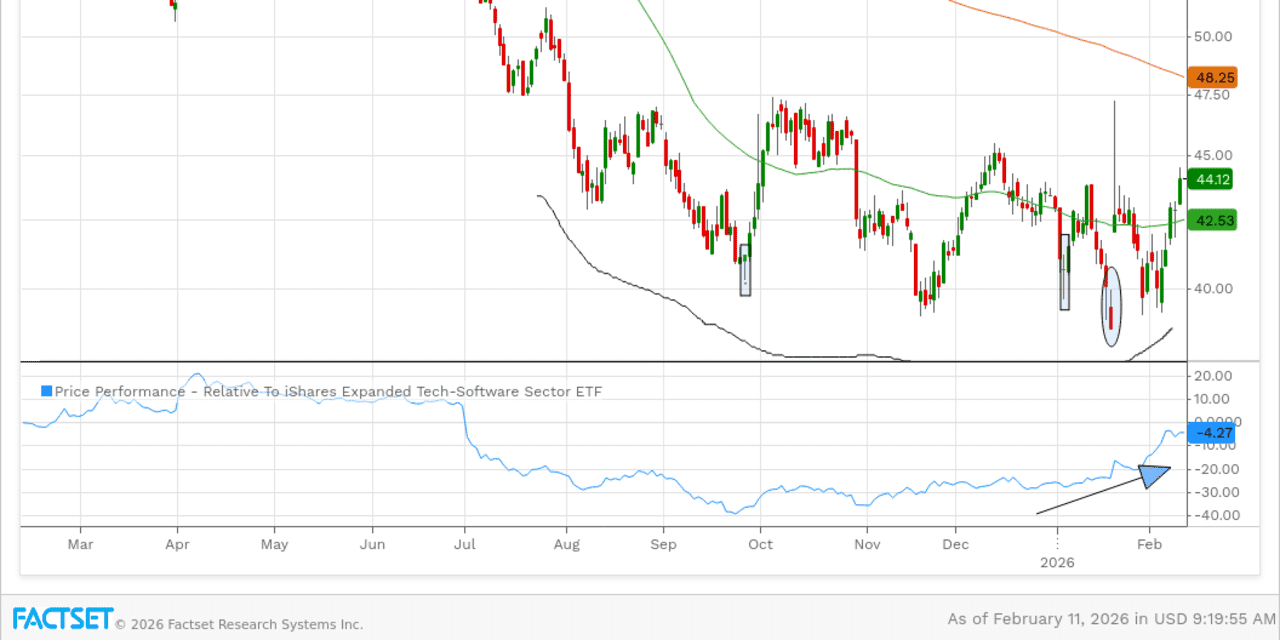

Market Trends Open New Avenues for 3 Previous Stock Selections: Technical Analysis

- Market Dynamics: The stock market is characterized by rapid changes, where previously popular stocks can quickly lose favor.

- Investor Strategy: Investors are increasingly looking back at former stock picks to identify potential opportunities for profit.

UBS Downgrades Crown Holdings to Neutral Amid Slowing Earnings Growth

- Earnings Growth Slowdown: UBS downgraded Crown Holdings (CCK) from Buy to Neutral, citing a slowdown in earnings growth as the beverage can maker ramps up investment to meet demand while operating near full capacity, with adjusted EPS growth expected to decline to about 6% over the next two years.

- High Capacity Utilization: While global beverage can demand remains strong, Crown (CCK) is operating close to full capacity, leading to pressures from startup costs and lower initial margins on new facilities, resulting in a 2% and 4% reduction in EPS forecasts for 2026 and 2027, respectively.

- Solid Cash Flow: Despite the weakening earnings momentum, UBS highlighted that Crown (CCK)'s cash generation remains a key support for the stock, estimating free cash flow of approximately $750 million annually, implying a free cash flow yield of about 5% that is expected to grow over time.

- Limited Valuation Upside: UBS maintained its $126 price target, applying a 9.5 times enterprise value to EBITDA multiple, with the stock trading near the upper end of Crown (CCK)'s recent valuation range, necessitating attention to risks from declining earnings or cost pressures.

Crown Holdings Reports Strong Q4 2025 Earnings with Strategic Outlook

- Significant Earnings Growth: Crown Holdings reported Q4 2025 earnings per share of $1.31, down from $3.02 in the prior year, yet adjusted EPS rose 9% to $1.74, showcasing the company's resilience and profitability in challenging conditions.

- Record Cash Flow: The company achieved a record free cash flow of $1.146 billion in 2025, up from $814 million in 2024, reflecting strong operational efficiency and capital management, providing a solid foundation for future investments and shareholder returns.

- Commitment to Strategic Investments: Management reiterated its focus on responsibly investing to support partners' growth while committing to gradually increasing dividends and returning $625 million to shareholders through disciplined share repurchases, highlighting its dedication to shareholder value.

- Optimistic Outlook: Crown Holdings projects adjusted EPS for 2026 to be between $1.70 and $1.80, with full-year free cash flow estimated at approximately $900 million, and despite challenges from inflation and start-up costs, management maintains a cautiously optimistic view on growth in North America and Europe.

Crown Holdings Announces 34.6% Increase in Quarterly Dividend

- Dividend Increase: Crown Holdings has declared a quarterly dividend increase from $0.26 to $0.35 per share, representing a 34.6% rise, which reflects the company's robust cash flow and profitability, thereby boosting investor confidence.

- Yield Metrics: Following this adjustment, the forward yield stands at 1.22%, which not only attracts income-seeking investors but also supports the company's performance in the capital markets.

- Shareholder Benefits: The dividend will be payable on March 31, with a record date of March 17 and an ex-dividend date also set for March 17, ensuring shareholders receive timely returns and reinforcing the relationship between the company and its investors.

- Future Projections: Crown Holdings projects earnings per share of $7.90 to $8.30 for 2026 while targeting $900 million in free cash flow through capacity expansions, demonstrating the company's confidence in future growth and strategic positioning.

CROWN HOLDINGS INC ANNOUNCES $0.35 PER SHARE CASH DIVIDEND PAYABLE ON MARCH 31, 2026

- Dividend Announcement: Crown Holdings Inc. has declared a cash dividend of $0.35 per share.

- Payment Date: The dividend is scheduled to be payable on March 31, 2026.

Amcor's Strategic Outlook Post-Berry Global Merger

- Merger Impact: Amcor's all-stock merger with Berry Global, completed last April, is projected to generate approximately $23 billion in revenue over the next twelve months, and if profit margins return to levels seen three years ago, net income could exceed $1.85 billion, highlighting the scale benefits and market potential of the merger.

- Earnings Guidance: Management has guided for adjusted earnings per share of $4.00 to $4.15 for FY2026, with free cash flow expected to be between $1.8 billion and $1.9 billion, indicating a strong financial outlook post-merger that could enhance investor confidence.

- Debt Management Risks: While the company aims to reduce its debt levels of approximately $15 billion, the current debt-to-EBITDA ratio stands at 4x, indicating potential operational leverage risks when paying down debt, especially as packaging demand may soften.

- Dividend Appeal: With a dividend yield of 5.24%, Amcor offers relative attractiveness in the current market, and while dividend payments may impact option pricing, the stable cash flow and dividend policy still provide value support for investors.

Market Trends Open New Avenues for 3 Previous Stock Selections: Technical Analysis

- Market Dynamics: The stock market is characterized by rapid changes, where previously popular stocks can quickly lose favor.

- Investor Strategy: Investors are increasingly looking back at former stock picks to identify potential opportunities for profit.

UBS Downgrades Crown Holdings to Neutral Amid Slowing Earnings Growth

- Earnings Growth Slowdown: UBS downgraded Crown Holdings (CCK) from Buy to Neutral, citing a slowdown in earnings growth as the beverage can maker ramps up investment to meet demand while operating near full capacity, with adjusted EPS growth expected to decline to about 6% over the next two years.

- High Capacity Utilization: While global beverage can demand remains strong, Crown (CCK) is operating close to full capacity, leading to pressures from startup costs and lower initial margins on new facilities, resulting in a 2% and 4% reduction in EPS forecasts for 2026 and 2027, respectively.

- Solid Cash Flow: Despite the weakening earnings momentum, UBS highlighted that Crown (CCK)'s cash generation remains a key support for the stock, estimating free cash flow of approximately $750 million annually, implying a free cash flow yield of about 5% that is expected to grow over time.

- Limited Valuation Upside: UBS maintained its $126 price target, applying a 9.5 times enterprise value to EBITDA multiple, with the stock trading near the upper end of Crown (CCK)'s recent valuation range, necessitating attention to risks from declining earnings or cost pressures.

Crown Holdings Reports Strong Q4 2025 Earnings with Strategic Outlook

- Significant Earnings Growth: Crown Holdings reported Q4 2025 earnings per share of $1.31, down from $3.02 in the prior year, yet adjusted EPS rose 9% to $1.74, showcasing the company's resilience and profitability in challenging conditions.

- Record Cash Flow: The company achieved a record free cash flow of $1.146 billion in 2025, up from $814 million in 2024, reflecting strong operational efficiency and capital management, providing a solid foundation for future investments and shareholder returns.

- Commitment to Strategic Investments: Management reiterated its focus on responsibly investing to support partners' growth while committing to gradually increasing dividends and returning $625 million to shareholders through disciplined share repurchases, highlighting its dedication to shareholder value.

- Optimistic Outlook: Crown Holdings projects adjusted EPS for 2026 to be between $1.70 and $1.80, with full-year free cash flow estimated at approximately $900 million, and despite challenges from inflation and start-up costs, management maintains a cautiously optimistic view on growth in North America and Europe.