Analysts Favor These 3 High-Dividend Stocks Amid Market Volatility

Market Volatility Concerns: Investors are increasingly worried about potential volatility in the stock market due to rising gold and silver prices, alongside fears of international sell-offs of U.S. assets, prompting a shift towards more defensive investment strategies.

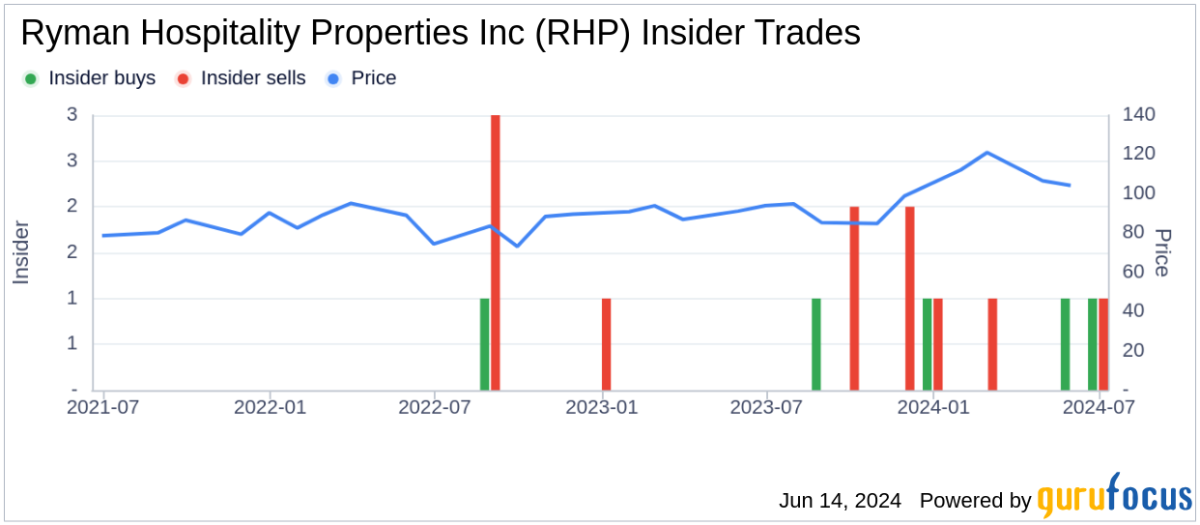

Ryman Hospitality Properties: Ryman Hospitality, focused on large hotel and resort investments, is noted for its strong dividend yield of 5.07% and a solid cash position, making it an attractive option for investors seeking dividend income.

Black Hills Corporation's Stability: Black Hills Corporation, a regulated utility company, offers reliable electric and natural gas services, with a dividend yield of 3.71% and a sustainable payout ratio, positioning it as a defensive investment in uncertain markets.

Essential Utilities Merger: Essential Utilities is set to merge with American Water Works, creating one of the largest U.S. water service firms, with expectations of significant earnings growth and a dividend yield of 3.55%, enhancing its appeal to investors.

Trade with 70% Backtested Accuracy

Analyst Views on RHP

About RHP

About the author

Ryman and Lakeland Executives Increase Stock Holdings

- RHP Stock Purchase: Colin V. Reed, Executive Chairman of Ryman Hospitality Properties, purchased 7,800 shares at $100.67 each on Friday, totaling $785,226, indicating strong confidence in the company's future prospects.

- Market Reaction: Despite Reed's purchase price being higher than Monday's trading low of $97.41, which is 3.2% below his purchase price, RHP's stock still rose about 0.3% on Monday, reflecting market recognition of its fundamentals.

- Welch's LKFN Purchase: M. Scott Welch, Director of Lakeland Financial, bought 10,000 shares at $57.95 each on Friday, totaling $579,500, demonstrating his optimism about the company's outlook.

- Historical Buying Activity: Prior to this latest purchase, Welch had invested a total of $920,374 in LKFN over the past year, with an average price of $61.36 per share, indicating his sustained belief in the company's long-term value.

Ryman Hospitality Successfully Prices $700 Million Senior Notes Offering

- Financing Size: Ryman Hospitality Properties successfully priced a $700 million offering of 5.750% senior notes, expected to close on March 11, 2026, indicating strong demand and financing capability in the capital markets.

- Use of Proceeds: The net proceeds from this issuance are anticipated to be approximately $687 million, which will be used to fully redeem the 4.750% senior notes due 2027, aimed at reducing interest burdens and optimizing the capital structure.

- Compliance: The notes will be sold only to qualified institutional buyers in compliance with Rule 144A under the Securities Act of 1933, ensuring the legality and compliance of the issuance while minimizing potential legal risks.

- Company Background: Ryman Hospitality is a leading lodging and hospitality REIT with 12,364 rooms and over 3 million square feet of meeting space, focusing on upscale convention center resorts, showcasing its significant position in the industry.

RHP Plans $700 Million Private Placement of Senior Notes

- Financing Plan: Ryman Hospitality Properties (RHP) announced that its subsidiaries intend to privately place $700 million of senior notes due 2034, aiming to enhance financial flexibility and optimize capital structure through this initiative.

- Use of Proceeds: The net proceeds from this offering will be used, along with available cash, to fully redeem the 4.750% senior notes due 2027, including accrued and unpaid interest and related fees, thereby reducing future interest burdens.

- Market Reaction: Following this announcement, RHP's stock price rose 0.75% in premarket trading to $103.6 per share, indicating a positive market response to the company's financial strategy.

- Future Outlook: RHP targets a 2.5% RevPAR growth for 2026 while planning to expand its group business and entertainment platform, demonstrating the company's proactive approach to seeking growth opportunities while maintaining stable cash flows.

Ryman Hospitality Properties Q4 2025 Earnings Call Highlights

- Performance Exceeds Expectations: Ryman Hospitality Properties reported Q4 2025 results that surpassed expectations, with the Entertainment segment and AFFO per share exceeding the upper end of guidance ranges, reflecting strong holiday programming and entertainment demand, thereby reinforcing the company's competitive position in the market.

- Acquisition and Expansion: The acquisition of JW Desert Ridge allows Ryman to enter a top 10 meetings market in the U.S., creating a second rotational pattern within the JW Marriott brand, which is expected to drive future revenue growth and increase market share.

- Liquidity and Financial Health: As of the end of Q4, the company had $471 million in unrestricted cash and total liquidity nearing $1.3 billion, demonstrating robust financial health that supports future investment opportunities.

- 2026 Outlook: Management anticipates a 2.5% growth in RevPAR and nearly 10% growth in Entertainment segment EBITDAre for 2026, with planned capital expenditures of $350 million to $450 million primarily in hospitality, showcasing confidence in future growth and strategic positioning.

Ryman Hospitality Properties Declares Quarterly Dividend of $1.20

- Quarterly Dividend Announcement: Ryman Hospitality Properties declares a quarterly dividend of $1.20 per share, consistent with previous distributions, indicating the company's stable cash flow and commitment to shareholder returns.

- Earnings Beat Expectations: The company's funds from operations (FFO) of $2.19 exceeded expectations by $0.02, demonstrating ongoing improvements in operational efficiency and profitability.

- Revenue Growth: RHP reported revenue of $737.81 million, surpassing market expectations by $21.73 million, reflecting strong performance and increasing customer demand in the market.

- Dividend Yield: The forward yield of 4.66% from this dividend appeals to income-seeking investors, further solidifying the company's attractiveness in the Real Estate Investment Trust (REIT) sector.

Ryman Hospitality Q4 FFO and Revenue Exceed Expectations

- Strong Financial Performance: Ryman Hospitality Properties reported a Q4 FFO of $2.19 per share, beating expectations by $0.02, indicating robust market performance that is likely to positively impact stock prices.

- Significant Revenue Growth: The company achieved Q4 revenue of $737.81 million, a 13.9% year-over-year increase, exceeding market expectations by $21.73 million, showcasing strong business momentum that may attract more investor interest.

- Optimistic Future Outlook: For 2026, the company projects same-store hospitality RevPAR growth between 1.50% and 3.50%, reflecting management's confidence in future market demand, which could drive long-term investment returns.

- Robust Adjusted EBITDA: The expected adjusted EBITDA ranges from $846 million to $895 million, demonstrating ongoing improvements in operational efficiency and profitability, further solidifying its competitive position in the industry.

Ryman and Lakeland Executives Increase Stock Holdings

- RHP Stock Purchase: Colin V. Reed, Executive Chairman of Ryman Hospitality Properties, purchased 7,800 shares at $100.67 each on Friday, totaling $785,226, indicating strong confidence in the company's future prospects.

- Market Reaction: Despite Reed's purchase price being higher than Monday's trading low of $97.41, which is 3.2% below his purchase price, RHP's stock still rose about 0.3% on Monday, reflecting market recognition of its fundamentals.

- Welch's LKFN Purchase: M. Scott Welch, Director of Lakeland Financial, bought 10,000 shares at $57.95 each on Friday, totaling $579,500, demonstrating his optimism about the company's outlook.

- Historical Buying Activity: Prior to this latest purchase, Welch had invested a total of $920,374 in LKFN over the past year, with an average price of $61.36 per share, indicating his sustained belief in the company's long-term value.

Ryman Hospitality Successfully Prices $700 Million Senior Notes Offering

- Financing Size: Ryman Hospitality Properties successfully priced a $700 million offering of 5.750% senior notes, expected to close on March 11, 2026, indicating strong demand and financing capability in the capital markets.

- Use of Proceeds: The net proceeds from this issuance are anticipated to be approximately $687 million, which will be used to fully redeem the 4.750% senior notes due 2027, aimed at reducing interest burdens and optimizing the capital structure.

- Compliance: The notes will be sold only to qualified institutional buyers in compliance with Rule 144A under the Securities Act of 1933, ensuring the legality and compliance of the issuance while minimizing potential legal risks.

- Company Background: Ryman Hospitality is a leading lodging and hospitality REIT with 12,364 rooms and over 3 million square feet of meeting space, focusing on upscale convention center resorts, showcasing its significant position in the industry.

RHP Plans $700 Million Private Placement of Senior Notes

- Financing Plan: Ryman Hospitality Properties (RHP) announced that its subsidiaries intend to privately place $700 million of senior notes due 2034, aiming to enhance financial flexibility and optimize capital structure through this initiative.

- Use of Proceeds: The net proceeds from this offering will be used, along with available cash, to fully redeem the 4.750% senior notes due 2027, including accrued and unpaid interest and related fees, thereby reducing future interest burdens.

- Market Reaction: Following this announcement, RHP's stock price rose 0.75% in premarket trading to $103.6 per share, indicating a positive market response to the company's financial strategy.

- Future Outlook: RHP targets a 2.5% RevPAR growth for 2026 while planning to expand its group business and entertainment platform, demonstrating the company's proactive approach to seeking growth opportunities while maintaining stable cash flows.

Ryman Hospitality Properties Q4 2025 Earnings Call Highlights

- Performance Exceeds Expectations: Ryman Hospitality Properties reported Q4 2025 results that surpassed expectations, with the Entertainment segment and AFFO per share exceeding the upper end of guidance ranges, reflecting strong holiday programming and entertainment demand, thereby reinforcing the company's competitive position in the market.

- Acquisition and Expansion: The acquisition of JW Desert Ridge allows Ryman to enter a top 10 meetings market in the U.S., creating a second rotational pattern within the JW Marriott brand, which is expected to drive future revenue growth and increase market share.

- Liquidity and Financial Health: As of the end of Q4, the company had $471 million in unrestricted cash and total liquidity nearing $1.3 billion, demonstrating robust financial health that supports future investment opportunities.

- 2026 Outlook: Management anticipates a 2.5% growth in RevPAR and nearly 10% growth in Entertainment segment EBITDAre for 2026, with planned capital expenditures of $350 million to $450 million primarily in hospitality, showcasing confidence in future growth and strategic positioning.

Ryman Hospitality Properties Declares Quarterly Dividend of $1.20

- Quarterly Dividend Announcement: Ryman Hospitality Properties declares a quarterly dividend of $1.20 per share, consistent with previous distributions, indicating the company's stable cash flow and commitment to shareholder returns.

- Earnings Beat Expectations: The company's funds from operations (FFO) of $2.19 exceeded expectations by $0.02, demonstrating ongoing improvements in operational efficiency and profitability.

- Revenue Growth: RHP reported revenue of $737.81 million, surpassing market expectations by $21.73 million, reflecting strong performance and increasing customer demand in the market.

- Dividend Yield: The forward yield of 4.66% from this dividend appeals to income-seeking investors, further solidifying the company's attractiveness in the Real Estate Investment Trust (REIT) sector.

Ryman Hospitality Q4 FFO and Revenue Exceed Expectations

- Strong Financial Performance: Ryman Hospitality Properties reported a Q4 FFO of $2.19 per share, beating expectations by $0.02, indicating robust market performance that is likely to positively impact stock prices.

- Significant Revenue Growth: The company achieved Q4 revenue of $737.81 million, a 13.9% year-over-year increase, exceeding market expectations by $21.73 million, showcasing strong business momentum that may attract more investor interest.

- Optimistic Future Outlook: For 2026, the company projects same-store hospitality RevPAR growth between 1.50% and 3.50%, reflecting management's confidence in future market demand, which could drive long-term investment returns.

- Robust Adjusted EBITDA: The expected adjusted EBITDA ranges from $846 million to $895 million, demonstrating ongoing improvements in operational efficiency and profitability, further solidifying its competitive position in the industry.