Cytokinetics Receives FDA Approval for MYQORZO, Driving Stock Surge

Cytokinetics Inc's stock surged by 8.64% as it reached a 5-day high, reflecting positive investor sentiment following recent developments.

The increase in stock price is attributed to Cytokinetics receiving FDA approval for MYQORZO (aficamten) to treat symptomatic obstructive hypertrophic cardiomyopathy (oHCM). This approval marks a significant milestone for the company, transitioning it from a development-stage biotech to a commercial entity. The approval is expected to enhance revenue prospects, addressing a critical gap in treatment options for oHCM patients.

This FDA approval not only boosts Cytokinetics' market position but also reflects the company's commitment to innovation in muscle biology. Investors are optimistic about the potential revenue growth as MYQORZO is anticipated to be available in the U.S. market soon.

Trade with 70% Backtested Accuracy

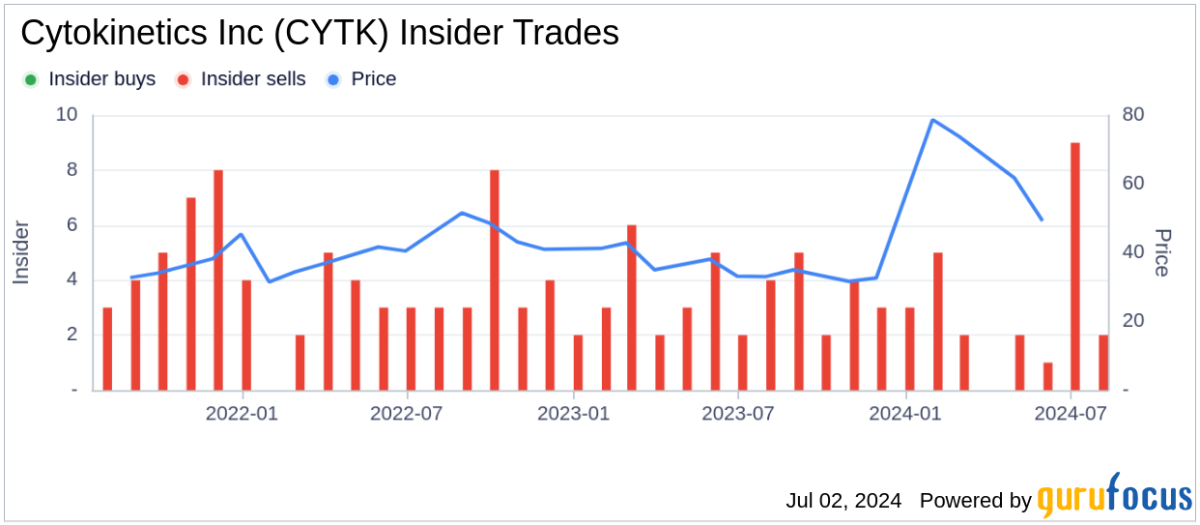

Analyst Views on CYTK

About CYTK

About the author

MongoDB and Warner Bros Options Trading Activity

- MongoDB Options Volume: As of now, MongoDB Inc's options volume has reached 12,327 contracts, equivalent to approximately 1.2 million shares, indicating a trading activity level that is 72.8% of its average daily volume over the past month, reflecting heightened market interest in the stock.

- High-Frequency Trading Insight: Notably, the $200 strike put option expiring on February 27, 2026, has seen a trading volume of 865 contracts today, representing about 86,500 underlying shares, which suggests investor expectations regarding future price volatility.

- Warner Bros Options Activity: Concurrently, Warner Bros Discovery Inc's options volume stands at 165,162 contracts, translating to approximately 16.5 million shares, which constitutes 70.4% of its average daily trading volume over the past month, indicating sustained market interest in the company.

- Bullish Call Options: For the $30 strike call option expiring on March 20, 2026, today's trading volume has reached 26,710 contracts, or about 2.7 million shares, reflecting investor optimism regarding Warner Bros' future performance.

Cytokinetics Q4 2025 Earnings Call Highlights

- FDA Approval Milestone: Cytokinetics achieved a significant milestone in Q4 2025 with the FDA approval of MYQORZO for symptomatic obstructive HCM, marking a successful transition from discovery to commercialization and enhancing its global market position.

- Market Promotion Strategy: CEO Blum emphasized the company's focus on implementing systems, education, and market access pathways to support physicians, patients, and payers, aiming for over 50% new patient preference share for MYQORZO by the end of 2026.

- Financial Performance Review: Total revenues for Q4 2025 reached $17.8 million, up from $16.9 million in the same period of 2024, although the net loss was $183 million, highlighting the financial challenges faced during market expansion.

- Future Outlook: CFO Lee indicated ongoing investments in R&D and marketing for 2026, and while no product sales guidance was provided, the launch of MYQORZO and the submission of the supplemental NDA for MAPLE-HCM are expected to lay the groundwork for future growth.

Cytokinetics (CYTK) Q4 2025 Earnings Transcript

Cytokinetics Q4 Earnings Report Analysis

- Earnings Performance: Cytokinetics reported a Q4 GAAP EPS of -$1.50, missing expectations by $0.05, indicating challenges in profitability that may affect investor confidence.

- Revenue Growth: The company achieved revenue of $17.75 million, a 4.8% year-over-year increase, beating market expectations by $9.73 million, suggesting improved market acceptance of its products and laying a foundation for future growth.

- 2026 Financial Guidance: Cytokinetics projects GAAP combined R&D and SG&A expenses for 2026 to be between $830 million and $870 million, including non-cash stock-based compensation expenses of $130 million to $120 million, reflecting the company's commitment to ongoing investment in R&D and marketing.

- FDA Approval Impact: The recent FDA approval of aficamten for hypertrophic cardiomyopathy may provide Cytokinetics with a new revenue stream, enhancing its competitive position in the cardiovascular drug market.

Cytokinetics' MYQORZO Approved and U.S. Launch Underway

- Drug Approval: Cytokinetics' MYQORZO (aficamten) received FDA approval in December 2025 for treating adults with symptomatic obstructive hypertrophic cardiomyopathy (oHCM), which is expected to significantly improve patients' functional capacity and symptoms, marking the company's transition into a commercial stage.

- Market Launch: The U.S. commercial launch of MYQORZO commenced in January 2026, with first prescriptions dispensed within days of drug availability, indicating the company's rapid response and strong momentum in market promotion.

- Financial Outlook: Cytokinetics anticipates combined R&D and SG&A expenses of $830 million to $870 million for 2026, demonstrating the company's commitment to advancing clinical trials and commercialization plans while maintaining approximately $1.2 billion in cash and investments.

- Clinical Trial Progress: The company plans to share topline results from ACACIA-HCM in Q2 2026 and launch MYQORZO in Germany, further enhancing its global market presence and business growth.

Cytokinetics to Announce Q4 Earnings on February 24

- Earnings Announcement: Cytokinetics (CYTK) is set to release its Q4 2023 earnings on February 24 after market close, with consensus EPS estimates at -$1.37 and revenue expectations at $8.02 million, reflecting a significant 52.6% year-over-year decline.

- Earnings Estimate Fluctuations: Over the past three months, EPS estimates have seen one upward revision and one downward adjustment, while revenue estimates have experienced three upward and three downward revisions, indicating market uncertainty regarding the company's future performance.

- FDA Approval Milestone: Cytokinetics recently received FDA approval for aficamten, a drug for hypertrophic cardiomyopathy, marking a significant advancement in the company's cardiac treatment portfolio, which could support future revenue growth.

- Market Attention: Cytokinetics presented at the 44th Annual J.P. Morgan Healthcare Conference, garnering investor interest and highlighting the company's potential and market confidence in the biopharmaceutical sector.

MongoDB and Warner Bros Options Trading Activity

- MongoDB Options Volume: As of now, MongoDB Inc's options volume has reached 12,327 contracts, equivalent to approximately 1.2 million shares, indicating a trading activity level that is 72.8% of its average daily volume over the past month, reflecting heightened market interest in the stock.

- High-Frequency Trading Insight: Notably, the $200 strike put option expiring on February 27, 2026, has seen a trading volume of 865 contracts today, representing about 86,500 underlying shares, which suggests investor expectations regarding future price volatility.

- Warner Bros Options Activity: Concurrently, Warner Bros Discovery Inc's options volume stands at 165,162 contracts, translating to approximately 16.5 million shares, which constitutes 70.4% of its average daily trading volume over the past month, indicating sustained market interest in the company.

- Bullish Call Options: For the $30 strike call option expiring on March 20, 2026, today's trading volume has reached 26,710 contracts, or about 2.7 million shares, reflecting investor optimism regarding Warner Bros' future performance.

Cytokinetics Q4 2025 Earnings Call Highlights

- FDA Approval Milestone: Cytokinetics achieved a significant milestone in Q4 2025 with the FDA approval of MYQORZO for symptomatic obstructive HCM, marking a successful transition from discovery to commercialization and enhancing its global market position.

- Market Promotion Strategy: CEO Blum emphasized the company's focus on implementing systems, education, and market access pathways to support physicians, patients, and payers, aiming for over 50% new patient preference share for MYQORZO by the end of 2026.

- Financial Performance Review: Total revenues for Q4 2025 reached $17.8 million, up from $16.9 million in the same period of 2024, although the net loss was $183 million, highlighting the financial challenges faced during market expansion.

- Future Outlook: CFO Lee indicated ongoing investments in R&D and marketing for 2026, and while no product sales guidance was provided, the launch of MYQORZO and the submission of the supplemental NDA for MAPLE-HCM are expected to lay the groundwork for future growth.

Cytokinetics (CYTK) Q4 2025 Earnings Transcript

Cytokinetics Q4 Earnings Report Analysis

- Earnings Performance: Cytokinetics reported a Q4 GAAP EPS of -$1.50, missing expectations by $0.05, indicating challenges in profitability that may affect investor confidence.

- Revenue Growth: The company achieved revenue of $17.75 million, a 4.8% year-over-year increase, beating market expectations by $9.73 million, suggesting improved market acceptance of its products and laying a foundation for future growth.

- 2026 Financial Guidance: Cytokinetics projects GAAP combined R&D and SG&A expenses for 2026 to be between $830 million and $870 million, including non-cash stock-based compensation expenses of $130 million to $120 million, reflecting the company's commitment to ongoing investment in R&D and marketing.

- FDA Approval Impact: The recent FDA approval of aficamten for hypertrophic cardiomyopathy may provide Cytokinetics with a new revenue stream, enhancing its competitive position in the cardiovascular drug market.

Cytokinetics' MYQORZO Approved and U.S. Launch Underway

- Drug Approval: Cytokinetics' MYQORZO (aficamten) received FDA approval in December 2025 for treating adults with symptomatic obstructive hypertrophic cardiomyopathy (oHCM), which is expected to significantly improve patients' functional capacity and symptoms, marking the company's transition into a commercial stage.

- Market Launch: The U.S. commercial launch of MYQORZO commenced in January 2026, with first prescriptions dispensed within days of drug availability, indicating the company's rapid response and strong momentum in market promotion.

- Financial Outlook: Cytokinetics anticipates combined R&D and SG&A expenses of $830 million to $870 million for 2026, demonstrating the company's commitment to advancing clinical trials and commercialization plans while maintaining approximately $1.2 billion in cash and investments.

- Clinical Trial Progress: The company plans to share topline results from ACACIA-HCM in Q2 2026 and launch MYQORZO in Germany, further enhancing its global market presence and business growth.

Cytokinetics to Announce Q4 Earnings on February 24

- Earnings Announcement: Cytokinetics (CYTK) is set to release its Q4 2023 earnings on February 24 after market close, with consensus EPS estimates at -$1.37 and revenue expectations at $8.02 million, reflecting a significant 52.6% year-over-year decline.

- Earnings Estimate Fluctuations: Over the past three months, EPS estimates have seen one upward revision and one downward adjustment, while revenue estimates have experienced three upward and three downward revisions, indicating market uncertainty regarding the company's future performance.

- FDA Approval Milestone: Cytokinetics recently received FDA approval for aficamten, a drug for hypertrophic cardiomyopathy, marking a significant advancement in the company's cardiac treatment portfolio, which could support future revenue growth.

- Market Attention: Cytokinetics presented at the 44th Annual J.P. Morgan Healthcare Conference, garnering investor interest and highlighting the company's potential and market confidence in the biopharmaceutical sector.