US Stocks Decline After Trump's Fed Chair Nomination

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jan 31 2026

0mins

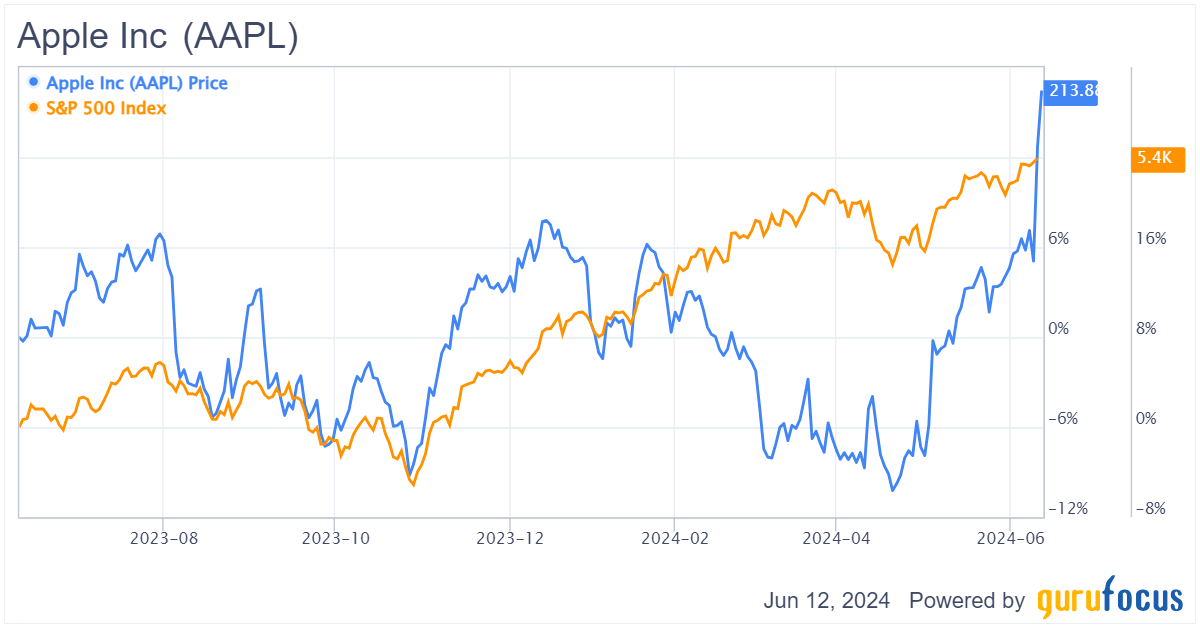

Should l Buy AAPL?

Source: Benzinga

- Increased Market Volatility: Trump's nomination of former Fed official Warsh as the new Fed chair unsettled investors, leading to significant declines in major indices as market participants reacted to heightened uncertainty regarding future monetary policy.

- Gold and Silver Plunge: Following Warsh's nomination, gold and silver experienced their steepest declines in decades, prompting investors to reassess monetary policy risks and resulting in a substantial loss of confidence among precious metal investors.

- Corporate Earnings Impact: Microsoft saw its shares drop sharply despite reporting better-than-expected earnings, as concerns over slowing Azure growth and cautious guidance weighed heavily on investor sentiment, contrasting with Meta's stock rally driven by strong advertising and engagement metrics.

- Rising Treasury Yields: As expectations for a more hawkish Fed stance grew, Treasury yields edged higher while equities retreated, and commodities lost significant recent gains, reflecting a cautious outlook among investors regarding the economic landscape ahead.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy AAPL?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on AAPL

Wall Street analysts forecast AAPL stock price to rise

27 Analyst Rating

17 Buy

9 Hold

1 Sell

Moderate Buy

Current: 263.750

Low

239.00

Averages

306.89

High

350.00

Current: 263.750

Low

239.00

Averages

306.89

High

350.00

About AAPL

Apple Inc. designs, manufactures and markets smartphones, personal computers, tablets, wearables and accessories, and sells a variety of related services. Its product categories include iPhone, Mac, iPad, and Wearables, Home and Accessories. Its software platforms include iOS, iPadOS, macOS, watchOS, visionOS, and tvOS. Its services include advertising, AppleCare, cloud services, digital content and payment services. The Company operates various platforms, including the App Store, that allow customers to discover and download applications and digital content, such as books, music, video, games and podcasts. It also offers digital content through subscription-based services, including Apple Arcade, Apple Fitness+, Apple Music, Apple News+, and Apple TV+. Its products include iPhone 16 Pro, iPhone 16, iPhone 15, iPhone 14, iPhone SE, MacBook Air, MacBook Pro, iMac, Mac mini, Mac Studio, Mac Pro, iPad Pro, iPad Air, AirPods, AirPods Pro, AirPods Max, Apple TV, Apple Vision Pro and others.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Apple's iPhone 17e Pricing Strategy Analysis

- Market Share Battle: In 2025, the iPhone became the top-selling smartphone, capturing 20% of the market share, and despite facing competitive pressures, Apple maintained high profits, demonstrating its strong competitive edge in the premium market.

- New Product Launch: At the spring event, Apple introduced the iPhone 17e with a starting price of $599, maintaining this price despite rising memory and storage chip costs, thereby attracting more consumers and enhancing market competitiveness.

- Supply Chain Advantage: Apple's strategy of securing multi-year agreements with suppliers allows it to manage price fluctuations effectively, ensuring production capacity and maintaining stable product pricing in a high-cost environment, further solidifying its market position.

- Long-term Shareholder Benefits: The pricing strategy of the iPhone 17e will enhance Apple's competitiveness in price-sensitive markets, likely attracting more users into the Apple ecosystem, which will promote sales of subsequent products and services, ultimately benefiting shareholders in the long run.

See More

China Sets Record Low GDP Growth Target for 2026

- GDP Growth Target: China has set its GDP growth target for 2026 at 4.5% to 5%, marking the lowest target on record since the early 1990s, indicating significant challenges for economic recovery amid persistent deflationary pressures and trade tensions with the U.S.

- Defense Spending Increase: Defense spending is projected to rise by 7%, the slowest increase since 2021, although analysts believe the official figures may be understated, which could impact national security and military modernization efforts.

- Data Center Attack: Amazon's data center in Bahrain was targeted by Iran for supporting the U.S. military, with damage reported from a drone strike, potentially affecting Amazon's cloud computing operations in the Middle East in the short term.

- Global Tariff Increase: U.S. Treasury Secretary announced that global tariffs will rise from 10% to 15%, with expectations that tariff rates will return to pre-Supreme Court ruling levels by August, which will have profound implications for international trade and the cost structures of U.S. businesses.

See More

Broadcom CEO Projects AI Chip Revenue Exceeding $100 Billion

- Surge in AI Revenue: Broadcom's AI revenue more than doubled year-over-year to $8.4 billion in Q1, contributing to a 29% increase in total sales to $19.3 billion, indicating strong demand and market potential in the AI sector.

- Strong Future Outlook: The company expects AI semiconductor revenue to reach $10.2 billion this quarter, with CEO Hock Tan projecting that AI chip revenue will significantly exceed $100 billion by 2027, reflecting confidence in future market growth.

- Rising Customer Demand: Broadcom is assisting six key customers, including Google, Meta, Anthropic, and OpenAI, in designing custom chips, showcasing the company's capability to meet the increasing demand for custom silicon from large clients.

- Supply Chain Assurance: Tan noted that the company has secured the supply chain necessary to achieve its 2027 sales targets, maintaining competitiveness in the AI accelerator market despite challenges such as high bandwidth memory shortages and manufacturing capacity constraints.

See More

Buffett's Investment Strategy and Holdings Analysis

- Long-Term Investment Philosophy: Over 60 years, Buffett achieved a compounded annual growth rate exceeding 19%, significantly outpacing the S&P 500's 10%, indicating the effectiveness of his investment strategy and its appeal to investors seeking inspiration.

- Apple Holdings: Buffett has held Apple shares since 2016, and despite selling some recently to lock in gains, it remains the largest holding in his portfolio, reflecting his ongoing confidence in the company and its strong brand moat.

- Coca-Cola's Steady Performance: Buffett has held Coca-Cola shares since the late 1980s, making it the fourth-largest holding in his portfolio; its status as a

See More

Three Stocks Reflecting Buffett's Investment Principles

- Apple's Stock Holding: Buffett has held Apple shares since 2016, witnessing an approximately 800% increase, and despite selling some shares last year, it remains the largest holding in his portfolio, indicating his ongoing confidence in the company.

- Coca-Cola's Long-Term Investment: Buffett has owned Coca-Cola stock since the late 1980s, making it the fourth-largest holding in his portfolio; its strong brand and global distribution network ensure steady earnings growth, complemented by over 50 years of dividend increases, showcasing its reliability.

- American Express's Robust Performance: Buffett's investment in American Express dates back to the 1960s, and it is now the second-largest holding in his portfolio, with 2023 revenues exceeding $72 billion, demonstrating resilience during economic fluctuations and making it a solid long-term investment choice.

- Buffett's Investment Wisdom: Buffett emphasizes long-term investing and selecting quality companies, with Apple, Coca-Cola, and American Express exemplifying this principle, allowing investors to adopt his strategy of choosing firms with competitive advantages for steady growth.

See More

Tech Industry Voices Concerns Over Supply Chain Risk Label

- Industry Response: The Information Technology Industry Council (ITI) sent a letter to Defense Secretary Pete Hegseth expressing concerns over his designation of a U.S. company as a supply chain risk, indirectly referencing Anthropic, which could jeopardize its future government contracts.

- Contract Dispute: ITI emphasized that contract disputes should be resolved through ongoing negotiations or by selecting alternative suppliers via established procurement channels rather than through emergency measures like supply chain risk designations, which are typically reserved for entities identified as foreign adversaries, reflecting strong opposition to government actions.

- Procedural Protections: The letter referenced the Federal Acquisition Supply Chain Security Act of 2018 and the Federal Acquisition Security Council (FASCSA), highlighting the importance of due process for private companies, including notice and response opportunities before any risk designation is made, underscoring ITI's commitment to procedural fairness.

- Anthropic's Position: Anthropic expressed deep sadness over the decision in a statement, arguing that labeling it as a supply chain risk is unprecedented and historically reserved for U.S. adversaries, which could severely impact its relationship with the Defense Department and the broader tech industry.

See More

Apple's iPhone 17e Pricing Strategy Analysis

- Market Share Battle: In 2025, the iPhone became the top-selling smartphone, capturing 20% of the market share, and despite facing competitive pressures, Apple maintained high profits, demonstrating its strong competitive edge in the premium market.

- New Product Launch: At the spring event, Apple introduced the iPhone 17e with a starting price of $599, maintaining this price despite rising memory and storage chip costs, thereby attracting more consumers and enhancing market competitiveness.

- Supply Chain Advantage: Apple's strategy of securing multi-year agreements with suppliers allows it to manage price fluctuations effectively, ensuring production capacity and maintaining stable product pricing in a high-cost environment, further solidifying its market position.

- Long-term Shareholder Benefits: The pricing strategy of the iPhone 17e will enhance Apple's competitiveness in price-sensitive markets, likely attracting more users into the Apple ecosystem, which will promote sales of subsequent products and services, ultimately benefiting shareholders in the long run.

See More

China Sets Record Low GDP Growth Target for 2026

- GDP Growth Target: China has set its GDP growth target for 2026 at 4.5% to 5%, marking the lowest target on record since the early 1990s, indicating significant challenges for economic recovery amid persistent deflationary pressures and trade tensions with the U.S.

- Defense Spending Increase: Defense spending is projected to rise by 7%, the slowest increase since 2021, although analysts believe the official figures may be understated, which could impact national security and military modernization efforts.

- Data Center Attack: Amazon's data center in Bahrain was targeted by Iran for supporting the U.S. military, with damage reported from a drone strike, potentially affecting Amazon's cloud computing operations in the Middle East in the short term.

- Global Tariff Increase: U.S. Treasury Secretary announced that global tariffs will rise from 10% to 15%, with expectations that tariff rates will return to pre-Supreme Court ruling levels by August, which will have profound implications for international trade and the cost structures of U.S. businesses.

See More

Broadcom CEO Projects AI Chip Revenue Exceeding $100 Billion

- Surge in AI Revenue: Broadcom's AI revenue more than doubled year-over-year to $8.4 billion in Q1, contributing to a 29% increase in total sales to $19.3 billion, indicating strong demand and market potential in the AI sector.

- Strong Future Outlook: The company expects AI semiconductor revenue to reach $10.2 billion this quarter, with CEO Hock Tan projecting that AI chip revenue will significantly exceed $100 billion by 2027, reflecting confidence in future market growth.

- Rising Customer Demand: Broadcom is assisting six key customers, including Google, Meta, Anthropic, and OpenAI, in designing custom chips, showcasing the company's capability to meet the increasing demand for custom silicon from large clients.

- Supply Chain Assurance: Tan noted that the company has secured the supply chain necessary to achieve its 2027 sales targets, maintaining competitiveness in the AI accelerator market despite challenges such as high bandwidth memory shortages and manufacturing capacity constraints.

See More

Buffett's Investment Strategy and Holdings Analysis

- Long-Term Investment Philosophy: Over 60 years, Buffett achieved a compounded annual growth rate exceeding 19%, significantly outpacing the S&P 500's 10%, indicating the effectiveness of his investment strategy and its appeal to investors seeking inspiration.

- Apple Holdings: Buffett has held Apple shares since 2016, and despite selling some recently to lock in gains, it remains the largest holding in his portfolio, reflecting his ongoing confidence in the company and its strong brand moat.

- Coca-Cola's Steady Performance: Buffett has held Coca-Cola shares since the late 1980s, making it the fourth-largest holding in his portfolio; its status as a

See More

Three Stocks Reflecting Buffett's Investment Principles

- Apple's Stock Holding: Buffett has held Apple shares since 2016, witnessing an approximately 800% increase, and despite selling some shares last year, it remains the largest holding in his portfolio, indicating his ongoing confidence in the company.

- Coca-Cola's Long-Term Investment: Buffett has owned Coca-Cola stock since the late 1980s, making it the fourth-largest holding in his portfolio; its strong brand and global distribution network ensure steady earnings growth, complemented by over 50 years of dividend increases, showcasing its reliability.

- American Express's Robust Performance: Buffett's investment in American Express dates back to the 1960s, and it is now the second-largest holding in his portfolio, with 2023 revenues exceeding $72 billion, demonstrating resilience during economic fluctuations and making it a solid long-term investment choice.

- Buffett's Investment Wisdom: Buffett emphasizes long-term investing and selecting quality companies, with Apple, Coca-Cola, and American Express exemplifying this principle, allowing investors to adopt his strategy of choosing firms with competitive advantages for steady growth.

See More

Tech Industry Voices Concerns Over Supply Chain Risk Label

- Industry Response: The Information Technology Industry Council (ITI) sent a letter to Defense Secretary Pete Hegseth expressing concerns over his designation of a U.S. company as a supply chain risk, indirectly referencing Anthropic, which could jeopardize its future government contracts.

- Contract Dispute: ITI emphasized that contract disputes should be resolved through ongoing negotiations or by selecting alternative suppliers via established procurement channels rather than through emergency measures like supply chain risk designations, which are typically reserved for entities identified as foreign adversaries, reflecting strong opposition to government actions.

- Procedural Protections: The letter referenced the Federal Acquisition Supply Chain Security Act of 2018 and the Federal Acquisition Security Council (FASCSA), highlighting the importance of due process for private companies, including notice and response opportunities before any risk designation is made, underscoring ITI's commitment to procedural fairness.

- Anthropic's Position: Anthropic expressed deep sadness over the decision in a statement, arguing that labeling it as a supply chain risk is unprecedented and historically reserved for U.S. adversaries, which could severely impact its relationship with the Defense Department and the broader tech industry.

See More