Qorvo (QRVO) Declines 10.3% Since Previous Earnings Report: Is a Recovery Possible?

Recent Performance: Qorvo's shares have declined by 10.3% since its last earnings report, underperforming the S&P 500, despite a strong Q2 fiscal 2026 performance where revenues and adjusted earnings exceeded estimates.

Earnings Highlights: The company reported a net income of $119.6 million, a significant turnaround from a loss in the previous year, driven by growth in the Advanced Cellular Group and High Performance Analog segments.

Future Projections: For Q3 fiscal 2026, Qorvo anticipates revenues of approximately $985 million, with non-GAAP earnings expected to be around $1.85 per share, indicating a positive outlook despite some challenges in the Connectivity and Sensors Group.

Market Sentiment: Analysts have raised their estimates for Qorvo, resulting in an 8.97% upward shift in consensus estimates, while the stock holds a Zacks Rank #3 (Hold), suggesting an expectation of stable returns in the near term.

Trade with 70% Backtested Accuracy

Analyst Views on QRVO

About QRVO

About the author

Starboard Value LP Acquires Stake in Fluor Corporation

- New Investment Activity: Starboard Value LP initiated a new position in Fluor Corporation (FLR) by acquiring 5,191,327 shares in Q4 2025, amounting to a total investment of $205.73 million, indicating confidence in Fluor's future growth prospects.

- Ownership Proportion Analysis: This acquisition accounts for 3.9% of Starboard's reportable AUM in its 13F filing, highlighting its significance within a diversified investment portfolio.

- Market Performance Review: As of February 17, 2026, Fluor's shares were priced at $48.57, reflecting a 22.2% increase over the past year, showcasing the company's recovery potential in the engineering and construction sector.

- Strategic Transformation Progress: Fluor has focused on restoring project discipline in recent years, shifting towards projects with more proportional risk structures, and if it can effectively manage project costs, it may enhance its profitability and cash flow stability.

Apple Launches iPhone 17e and Updated iPad Air

- Launch of iPhone 17e: Apple has introduced the iPhone 17e, starting at $599 as a budget model in the iPhone 17 lineup, maintaining a 6.1-inch size while featuring tougher glass, the A19 chip, and 256GB of base storage, enhancing its competitiveness in the budget market.

- iPad Air Upgrade: The updated iPad Air retains its design and pricing but upgrades from the M3 to the M4 chip, with the 11-inch model starting at $599 and the 13-inch version at $799, while the M4 chip offers up to 30% faster performance, increasing its market appeal.

- Preorder and Availability: Preorders for the iPhone 17e will begin on March 4, with in-store availability starting on March 11, a strategic timing aimed at maximizing market response and meeting consumer demand effectively.

- Future Product Announcements: Apple plans to unveil more products in the coming days, which is expected to generate significant consumer excitement, further driving sales growth and enhancing brand influence.

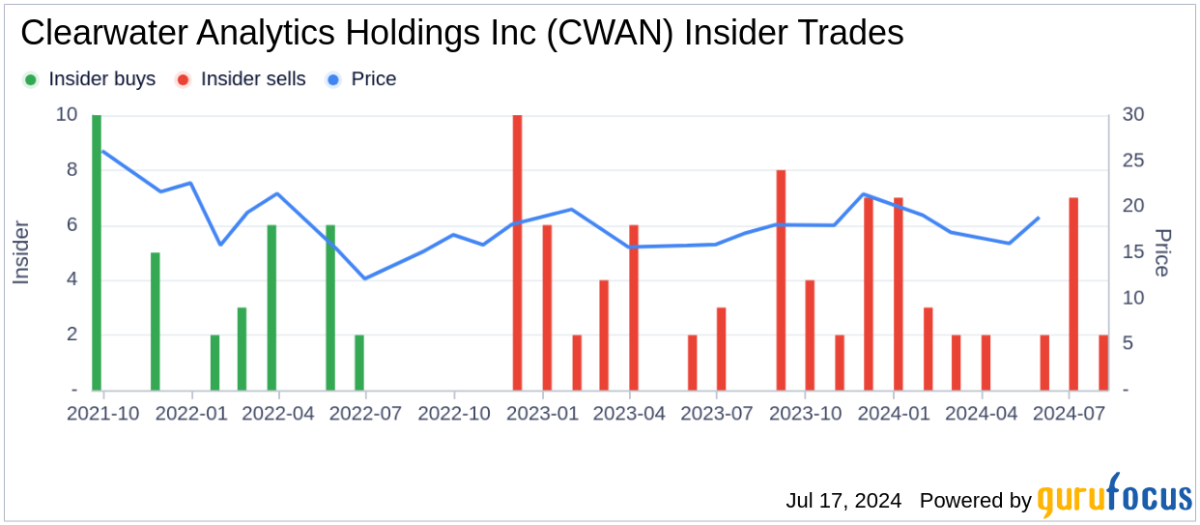

Starboard Value LP Acquires Stake in Clearwater Analytics

- New Investment Disclosure: According to a February 17, 2026 SEC filing, Starboard Value LP disclosed a new position in Clearwater Analytics by purchasing 9,959,031 shares valued at $240.21 million, indicating confidence in the company's growth potential.

- Asset Management Proportion: This acquisition represents 4.55% of Starboard's reportable assets under management as of December 31, 2025, highlighting the importance of Clearwater in their investment strategy and potentially influencing future allocations.

- Market Performance Analysis: As of February 17, 2026, Clearwater's shares were priced at $22.93, reflecting a 17% decline over the past year and underperforming the S&P 500 by 26.7 percentage points, which suggests market caution regarding its growth outlook.

- Business Model and Challenges: Clearwater Analytics focuses on providing automated investment data management solutions for institutional clients; while its cloud platform ensures steady recurring revenue, the complexity of client onboarding may slow margin growth, prompting investors to assess whether revenue can outpace service delivery costs.

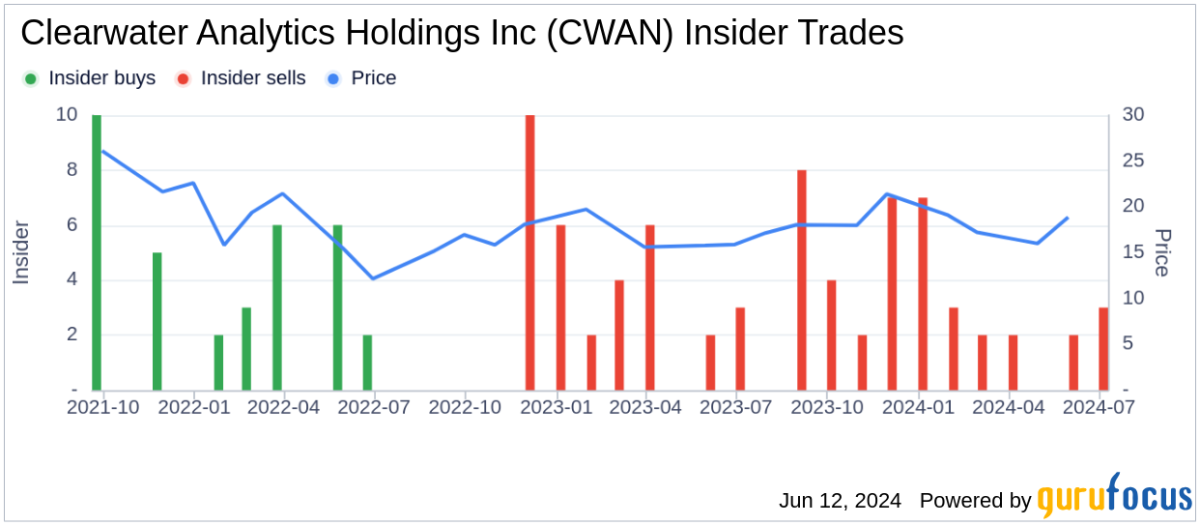

Starboard Value Acquires Stake in Clearwater Analytics

- Acquisition Overview: Starboard Value LP acquired 9,959,031 shares in Clearwater Analytics, with an estimated transaction value of $240.21 million, reflecting a new position in its investment portfolio.

- Asset Management Proportion: The newly acquired stake represents 4.55% of Starboard's 13F reportable assets under management, indicating a significant investment despite not being among the top five holdings.

- Market Performance Analysis: As of February 17, 2026, Clearwater Analytics shares were priced at $22.93, down 17% over the past year, underperforming the S&P 500 by 26.7 percentage points, raising concerns about its growth potential.

- Business Model and Challenges: Clearwater Analytics focuses on providing SaaS solutions for automated investment data management, ensuring stable recurring revenue through its subscription model, but the client onboarding process may slow margin growth, making future growth reliant on deeper usage by existing clients.

Starboard Value LP Acquires Major Stake in Clearwater Analytics

- New Investment Disclosure: On February 17, 2026, Starboard Value LP disclosed a purchase of 9,959,031 shares in Clearwater Analytics, valued at $240.21 million, indicating a significant new investment that could influence market performance.

- Asset Management Proportion: This acquisition represents 4.55% of Starboard's reportable assets under management as of December 31, 2025, highlighting Clearwater's importance in its portfolio and potentially attracting more investor interest.

- Market Performance Analysis: As of February 17, 2026, Clearwater's shares were priced at $22.93, down 17.0% over the past year and underperforming the S&P 500 by 26.7 percentage points, reflecting market concerns about its future growth prospects.

- Business Model and Challenges: Clearwater Analytics focuses on automated investment data management, and while its cloud platform provides steady recurring revenue, the complexities of client onboarding and data integration may hinder margin growth, prompting investors to monitor whether revenue growth can outpace service delivery costs.

Jim Cramer Highlights AI Investment Opportunities

- AI Investment Focus: Jim Cramer emphasized the significance of AI stocks during the Investing Club meeting, particularly highlighting Nvidia as the gold standard in AI computing, with its stunning quarterly results reinforcing the notion of an ongoing Fourth Industrial Revolution.

- Corning's New Strategy: After visiting its Kentucky factory, Jim learned about Corning's ambition to enhance data center connectivity by replacing copper with fiber optics, indicating a strong growth trajectory in the data center market that could drive future company performance.

- Eaton's Acquisition Plans: Eaton's strategy to spin off its eMobility unit and acquire Boyd Thermal aims to bolster its competitive edge in liquid cooling technology, which is crucial for managing heat in AI chips, thereby enhancing its market position.

- Alphabet and Amazon Performance: Alphabet stands out in the AI sector with its strong YouTube and cloud computing divisions, while Amazon's AWS cloud business is accelerating, although both face capital expenditure pressures, they are still viewed as solid long-term investment opportunities.

Starboard Value LP Acquires Stake in Fluor Corporation

- New Investment Activity: Starboard Value LP initiated a new position in Fluor Corporation (FLR) by acquiring 5,191,327 shares in Q4 2025, amounting to a total investment of $205.73 million, indicating confidence in Fluor's future growth prospects.

- Ownership Proportion Analysis: This acquisition accounts for 3.9% of Starboard's reportable AUM in its 13F filing, highlighting its significance within a diversified investment portfolio.

- Market Performance Review: As of February 17, 2026, Fluor's shares were priced at $48.57, reflecting a 22.2% increase over the past year, showcasing the company's recovery potential in the engineering and construction sector.

- Strategic Transformation Progress: Fluor has focused on restoring project discipline in recent years, shifting towards projects with more proportional risk structures, and if it can effectively manage project costs, it may enhance its profitability and cash flow stability.

Apple Launches iPhone 17e and Updated iPad Air

- Launch of iPhone 17e: Apple has introduced the iPhone 17e, starting at $599 as a budget model in the iPhone 17 lineup, maintaining a 6.1-inch size while featuring tougher glass, the A19 chip, and 256GB of base storage, enhancing its competitiveness in the budget market.

- iPad Air Upgrade: The updated iPad Air retains its design and pricing but upgrades from the M3 to the M4 chip, with the 11-inch model starting at $599 and the 13-inch version at $799, while the M4 chip offers up to 30% faster performance, increasing its market appeal.

- Preorder and Availability: Preorders for the iPhone 17e will begin on March 4, with in-store availability starting on March 11, a strategic timing aimed at maximizing market response and meeting consumer demand effectively.

- Future Product Announcements: Apple plans to unveil more products in the coming days, which is expected to generate significant consumer excitement, further driving sales growth and enhancing brand influence.

Starboard Value LP Acquires Stake in Clearwater Analytics

- New Investment Disclosure: According to a February 17, 2026 SEC filing, Starboard Value LP disclosed a new position in Clearwater Analytics by purchasing 9,959,031 shares valued at $240.21 million, indicating confidence in the company's growth potential.

- Asset Management Proportion: This acquisition represents 4.55% of Starboard's reportable assets under management as of December 31, 2025, highlighting the importance of Clearwater in their investment strategy and potentially influencing future allocations.

- Market Performance Analysis: As of February 17, 2026, Clearwater's shares were priced at $22.93, reflecting a 17% decline over the past year and underperforming the S&P 500 by 26.7 percentage points, which suggests market caution regarding its growth outlook.

- Business Model and Challenges: Clearwater Analytics focuses on providing automated investment data management solutions for institutional clients; while its cloud platform ensures steady recurring revenue, the complexity of client onboarding may slow margin growth, prompting investors to assess whether revenue can outpace service delivery costs.

Starboard Value Acquires Stake in Clearwater Analytics

- Acquisition Overview: Starboard Value LP acquired 9,959,031 shares in Clearwater Analytics, with an estimated transaction value of $240.21 million, reflecting a new position in its investment portfolio.

- Asset Management Proportion: The newly acquired stake represents 4.55% of Starboard's 13F reportable assets under management, indicating a significant investment despite not being among the top five holdings.

- Market Performance Analysis: As of February 17, 2026, Clearwater Analytics shares were priced at $22.93, down 17% over the past year, underperforming the S&P 500 by 26.7 percentage points, raising concerns about its growth potential.

- Business Model and Challenges: Clearwater Analytics focuses on providing SaaS solutions for automated investment data management, ensuring stable recurring revenue through its subscription model, but the client onboarding process may slow margin growth, making future growth reliant on deeper usage by existing clients.

Starboard Value LP Acquires Major Stake in Clearwater Analytics

- New Investment Disclosure: On February 17, 2026, Starboard Value LP disclosed a purchase of 9,959,031 shares in Clearwater Analytics, valued at $240.21 million, indicating a significant new investment that could influence market performance.

- Asset Management Proportion: This acquisition represents 4.55% of Starboard's reportable assets under management as of December 31, 2025, highlighting Clearwater's importance in its portfolio and potentially attracting more investor interest.

- Market Performance Analysis: As of February 17, 2026, Clearwater's shares were priced at $22.93, down 17.0% over the past year and underperforming the S&P 500 by 26.7 percentage points, reflecting market concerns about its future growth prospects.

- Business Model and Challenges: Clearwater Analytics focuses on automated investment data management, and while its cloud platform provides steady recurring revenue, the complexities of client onboarding and data integration may hinder margin growth, prompting investors to monitor whether revenue growth can outpace service delivery costs.

Jim Cramer Highlights AI Investment Opportunities

- AI Investment Focus: Jim Cramer emphasized the significance of AI stocks during the Investing Club meeting, particularly highlighting Nvidia as the gold standard in AI computing, with its stunning quarterly results reinforcing the notion of an ongoing Fourth Industrial Revolution.

- Corning's New Strategy: After visiting its Kentucky factory, Jim learned about Corning's ambition to enhance data center connectivity by replacing copper with fiber optics, indicating a strong growth trajectory in the data center market that could drive future company performance.

- Eaton's Acquisition Plans: Eaton's strategy to spin off its eMobility unit and acquire Boyd Thermal aims to bolster its competitive edge in liquid cooling technology, which is crucial for managing heat in AI chips, thereby enhancing its market position.

- Alphabet and Amazon Performance: Alphabet stands out in the AI sector with its strong YouTube and cloud computing divisions, while Amazon's AWS cloud business is accelerating, although both face capital expenditure pressures, they are still viewed as solid long-term investment opportunities.